The year of the rabbit (and the REIT?)

Article4 Minutes07 March 2023

According to the Chinese calendar, 2023 is the year of the rabbit. History suggests it could also be the year of the REIT.

Last year was a tough one for investors in real estate investment trusts (REITs). The potent mix of the war in Ukraine, surging inflation and central banks raising interest rates, created an unpredictable investment environment.

This was reflected in the performance of global REITs. In 2021, as markets stabilised following COVID-19, global REITS delivered a total return of 47% (GPR 250 REIT Index (US)). In 2022, the sector fell 25%. So, what does 2023 have in store?

Let’s attempt to answer that question by first looking over our shoulders. The speed and severity of last year’s decline was largely a result of increasing interest rates which, most simplistically, negatively impacts real estate valuations.

At the same time, the yield on 10-year US Treasuries rose by a factor of 2.5, heralding a material regime change in the investing environment.

For more than a decade, investors had become accustomed to historically low rates. Now, primarily driven by inflation, the era of highly stimulatory, lower-for-longer interest rates is over, resulting in a step-change in financial and investor markets.

This step-change negatively impacted REITs, as rising rates provided more choice to investors through higher bond yields while simultaneously negatively impacting real estate valuations.

As long-term investors specialising in listed real estate securities, we have seen these cycles before. But history suggests these periods can also offer incredibly fertile investment opportunities.

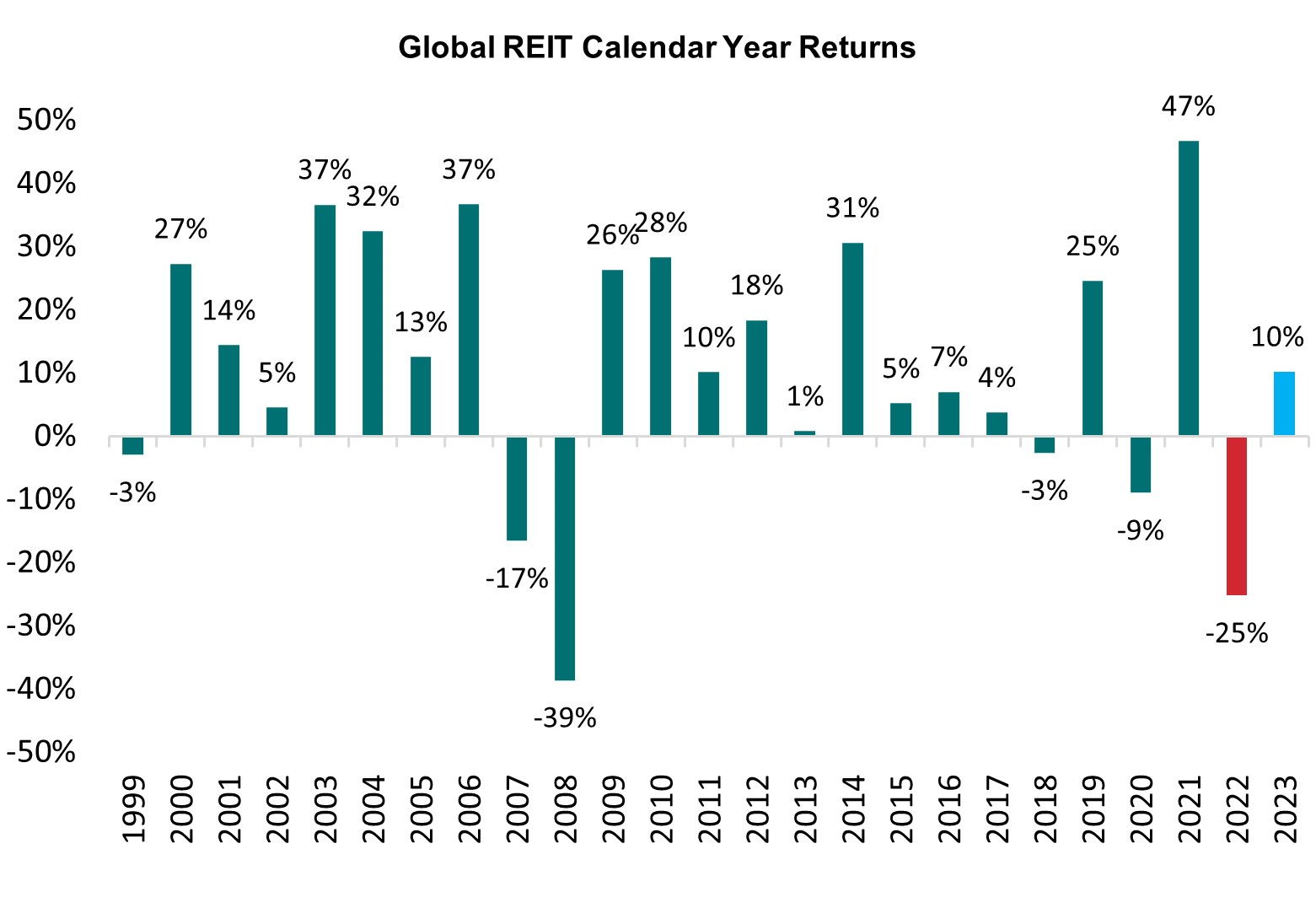

This chart shows global REIT calendar year returns since 1999.

Source: DXAM, Bloomberg, GPR USD TR Used as Global REIT proxy

Global REIT returns have been positive in 18 of the past 24 years. On all but one occasion - the global financial crisis - positive returns were posted following each negative year.

This year has so far followed a similar pattern. After the 25% fall last year, global REITs were up 10% in January. The conclusion is as obvious as it is alluring. Throughout the most recent two decades, investors have done particularly well entering the sector when share prices have fallen significantly.

With a focus on net asset value and share price returns from the GFC and COVID-19 periods (when major pullbacks occurred), we analysed almost 300 individual global REITs data points to better understand the relative share price performance.

Source: DXAM, Bloomberg, GPR250 USD TR Used as Global REIT proxy

As can be seen, there is a strong positive relationship (R-square of 0.3084) between Global REITs’ discount to net asset value (NAV) and the forward one-year share price return over the GFC and COVID-19 periods. On average, the data suggests that a trough discount-to-NAV of circa 27% was followed by a one-year forward share price return of over 70%.

It is dangerous and unrealistic to suggest past returns are in any way an indication of future performance, especially when the outlook for Global REITs remains uncertain (see below). That said, this finding does support one of the founding principles of how we like to invest; when you buy something below fair value, your long-term returns tend to thank you for it.

Challenging conditions

So, what of the future? The developed world is concerned with inflation, especially in Europe where energy costs are biting. The consensus is for an economic slowdown this year, with many just waiting for technical confirmation of it.

The depth and duration of any downturn is impossible to know but the range of views can be segregated into two camps. The optimistic cohort point to above-full employment and strong consumer spending, while the bearish worry about the prospect of stagflation (high inflation and weak economic conditions).

There are signs inflation is already falling but the lag effect of policy rate increases has yet to fully play out. Inevitably, this involves some guesswork on the part of central bankers. And we will have to wait and see if the increases over the past 12 months were overcooked, or if there will be a requirement for more.

Either way, the rate outlook is uncertain and the conditions challenging. Until rates stabilise, transaction activity is likely to be low as investment decisions are postponed and projects are delayed. There may even be forced sales as interest servicing costs bite and/or lenders become skittish over gearing levels.

Perhaps counterintuitively, this bodes well for commercial property investors. This is a market where predictable and attractive yields are likely to become more highly prized than they were in 2022.

Global REITs are amongst the best capitalised real estate ownership vehicles in the market. They also own some of the highest quality assets, delivering attractive dividend yields from high-quality portfolios and cycle-tested management teams.

Select global REITs like those featured in the Dexus Global REIT Fund have the potential to provide investors with liquid access to a defensive real asset class with inflation-protection characteristics. Best of all, right now many are available at appealing prices.

After a tough 2022, the outlook for REIT investors in 2023 surely looks better.

Disclaimer:

This material (“Material”) has been prepared by Dexus Asset Management Limited (ACN 080 674 479, AFSL No. 237500) (“DXAM”), the responsible entity and issuer of the financial products of Dexus Global REIT Fund (ARSN 642 411 292) mentioned in this Material. DXAM is a wholly owned subsidiary of Dexus (ASX: DXS).

Information in this Material is current as at 20 February 2023 (unless otherwise indicated), is for general information purposes only, (subject to applicable law) does not constitute financial product advice, has been prepared without taking account of the recipient’s objectives, financial situation and needs, and does not purport to contain all information necessary for making an investment decision. Accordingly, and before you receive any financial service from us (including deciding to acquire or to continue to hold a product in any fund mentioned in this Material), or act on this Material, investors should obtain and consider the relevant product disclosure statement (“PDS”), DXAM financial services guide (“FSG”) and relevant target market determination (“TMD”) in full, consider the appropriateness of this Material having regard to your own objectives, financial situation and needs and seek independent legal, tax and financial advice. The PDS, FSG and TMD (hard copy or electronic copy) are available from DXAM, Level 5, 80 Collins Street (South Tower), Melbourne VIC 3000, by visiting https://www.dexus.com/investor-centre, by emailing investorservices@dexus.com or by phoning 1800 996 456. The PDS contains important information about risks, costs and fees (including fees payable to DXAM for managing the fund). Any investment is subject to investment risk, including possible delays in repayment and loss of income and principal invested, and there is no guarantee on the performance of the fund or the return of any capital. This Material does not constitute an offer, invitation, solicitation or recommendation to subscribe for, purchase or sell any financial product, and does not form the basis of any contract or commitment. This Material must not be reproduced or used by any person without DXAM’s prior written consent. This Material is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives.

Any forward looking statements, opinions and estimates (including statements of intent) in this Material are based on estimates and assumptions related to future business, economic, market, political, social and other conditions that are inherently subject to significant uncertainties, risks and contingencies, and the assumptions may change at any time without notice. Actual results may differ materially from those predicted or implied by any forward looking statements for a range of reasons. Past performance is not an indication of future performance. The forward looking statements only speak as at the date of this Material, and except as required by law, DXAM disclaims any duty to update them to reflect new developments.

Except as required by law, no representation, assurance, guarantee or warranty, express or implied, is made as to the fairness, authenticity, validity, suitability, reliability, accuracy, completeness or correctness of any information, statement, estimate or opinion, or as to the reasonableness of any assumption, in this Material. By reading or viewing this Material and to the fullest extent permitted by law, the recipient releases Dexus, DXAM, their affiliates, and all of their directors, officers, employees, representatives and advisers from any and all direct, indirect and consequential losses, damages, costs, expenses and liabilities of any kind (“Losses”) arising in connection with any recipient or person acting on or relying on anything contained in or omitted from this Material or any other written or oral information, statement, estimate or opinion, whether or not the Losses arise in connection with any negligence or default of Dexus, DXAM or their affiliates, or otherwise.

Dexus, DXAM and/or their affiliates may have an interest in the financial products, and may earn fees as a result of transactions, mentioned in this Material.